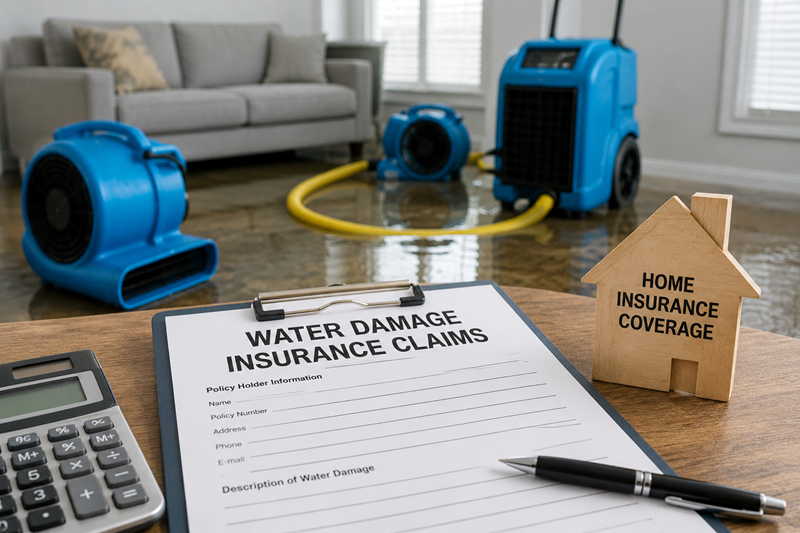

Water damage is one of the most common reasons homeowners file insurance claims in the United States. Whether caused by a burst pipe, overflowing appliance, roof leak, or severe storm, unexpected water intrusion can quickly lead to structural damage, mold growth, and costly repairs. Understanding Water Damage Insurance Claims is essential for homeowners who want to protect their property and recover financially after a covered loss. Insurance policies have evolved alongside changing weather patterns, rising repair costs, and stricter documentation requirements, making it more important than ever to know what your policy covers and how to navigate the claims process effectively.

According to the Insurance Information Institute (Triple-I), water damage and freezing remain among the leading causes of homeowner insurance losses, accounting for billions of dollars in property damage each year. While insurance can provide valuable financial protection, successful claims often depend on prompt action, accurate documentation, and a clear understanding of policy terms.

Why Water Damage Insurance Claims Matter More in 2026

In recent years, homeowners across the United States have experienced an increase in severe weather events, aging plumbing systems, and costly home repairs. These factors have made water damage one of the most expensive and disruptive property issues.

Insurance providers are also placing greater emphasis on:

- Thorough documentation.

- Preventive home maintenance.

- Timely claim reporting.

- Professional damage assessments.

- Accurate repair estimates.

As a result, homeowners who understand the claims process are often better prepared to avoid delays and reduce the likelihood of disputes.

What Is Considered Water Damage?

Water damage refers to physical damage caused when water enters areas where it should not be. The source of the water often determines whether insurance coverage applies.

Common examples include:

- Burst or frozen pipes.

- Overflowing washing machines or dishwashers.

- Sudden plumbing failures.

- Water heater leaks.

- Roof leaks caused by storms.

- Wind-driven rain entering through storm-damaged roofs.

- Accidental sprinkler system discharge.

- Ice dam damage in colder climates.

Water can damage:

- Drywall.

- Hardwood flooring.

- Carpets.

- Cabinets.

- Insulation.

- Electrical systems.

- Personal belongings.

- Furniture.

- Structural framing.

Even a small leak can lead to hidden moisture behind walls, increasing the risk of mold growth if left untreated.

What Does Homeowners Insurance Usually Cover?

Although every insurance policy is different, most standard homeowners insurance policies generally cover sudden and accidental water damage.

Examples of commonly covered events include:

Burst Pipes

If a pipe suddenly bursts due to freezing temperatures or an unexpected plumbing failure, the resulting damage is often covered.

Appliance Failures

Unexpected leaks from appliances such as:

- Washing machines.

- Refrigerators.

- Water heaters.

- Dishwashers.

may qualify for coverage if they occur suddenly.

Storm-Related Water Damage

If strong winds damage your roof and rain enters your home afterward, many policies cover the resulting interior damage.

Accidental Plumbing Overflows

Overflowing sinks, bathtubs, or toilets caused by accidental plumbing issues may also be covered depending on the policy language.

What Is Commonly Excluded?

Many homeowners are surprised to learn that not every type of water damage is covered.

Common exclusions include:

Flood Damage

Flooding caused by rising rivers, storm surge, or heavy surface water generally requires a separate flood insurance policy.

Long-Term Leaks

Insurance may deny claims if damage resulted from:

- Slow plumbing leaks

- Neglected maintenance

- Worn-out seals

- Continuous water seepage

These situations are often considered preventable maintenance issues rather than sudden accidents.

Sewer Backup

Many insurers require an additional endorsement for sewer or drain backup coverage.

Groundwater Intrusion

Water entering through foundation cracks or basement walls due to groundwater pressure is frequently excluded.

Understanding these exclusions before a loss occurs can help homeowners avoid unexpected financial responsibilities.

The First Steps to Take After Discovering Water Damage

The actions taken during the first few hours can influence both the extent of property damage and the outcome of an insurance claim.

1. Stop the Water Source

If possible, turn off the main water supply or shut down the appliance causing the leak.

2. Ensure Safety

Avoid standing water near electrical outlets or damaged wiring. If necessary, switch off electricity to affected areas.

3. Document Everything

Before moving belongings or beginning cleanup:

- Take clear photographs.

- Record videos.

- Capture close-up and wide-angle images.

- Document damaged furniture and personal items.

This evidence can help support your claim.

4. Prevent Additional Damage

Most insurance policies require homeowners to take reasonable steps to prevent further damage.

Examples include:

- Placing tarps over roof openings.

- Removing standing water.

- Using fans or dehumidifiers if safe.

- Moving valuables to dry areas.

Keep receipts for emergency expenses, as some policies may reimburse these costs.

How to File Water Damage Insurance Claims Successfully

Filing a claim involves more than simply notifying your insurance company. A well-organized approach can help streamline the process.

Contact Your Insurance Company Promptly

Report the incident as soon as possible. Delays could complicate the investigation or affect coverage.

Be prepared to provide:

- Policy number.

- Date and time of the incident.

- Cause of the damage (if known).

- Photos and videos.

- Emergency mitigation steps already taken.

Schedule an Inspection

An insurance adjuster will typically inspect the property to assess the damage and determine coverage under your policy.

During the inspection:

- Walk through every affected area.

- Share all documentation.

- Point out hidden or less obvious damage.

- Ask questions about the next steps in the claims process.

Maintain Detailed Records

Keep copies of:

- Emails.

- Claim numbers.

- Repair estimates.

- Contractor invoices.

- Temporary repair receipts.

- Communication with your insurer.

Organized documentation can help resolve questions more efficiently if they arise.

Why Professional Water Mitigation Can Support Your Claim

While homeowners may handle small cleanups, significant water damage often requires specialized drying equipment and moisture detection tools.

Professional mitigation companies typically:

- Extract standing water.

- Measure hidden moisture.

- Dry structural materials.

- Document moisture readings.

- Produce detailed restoration reports.

- Help reduce the risk of mold growth.

These records can provide additional evidence of the extent of the damage and the mitigation steps taken, which may assist during the insurance review process.

Common Reasons Water Damage Insurance Claims Are Denied

Not every claim results in a payout. Insurance companies evaluate whether the damage is covered under the policy and whether the homeowner fulfilled their responsibilities. Understanding the most common reasons for claim denials can help you avoid costly mistakes.

1. Delayed Claim Reporting

Waiting days or weeks to report water damage can make it difficult to determine the original cause of the loss. Most insurance policies require policyholders to notify their insurer promptly after discovering the damage.

2. Lack of Documentation

Photos, videos, receipts, and repair estimates are essential when supporting a claim. Without sufficient evidence, insurers may have difficulty verifying the extent of the damage or the value of damaged belongings.

3. Poor Home Maintenance

Insurance generally covers sudden and accidental events—not damage caused by neglect. Claims may be denied if the insurer determines the problem resulted from:

- Aging or corroded plumbing

- Long-term roof leaks

- Poorly maintained appliances

- Ignored moisture problems

Routine inspections and timely repairs can help reduce this risk.

4. Damage Outside Policy Coverage

Many homeowners assume every type of water damage is insured. However, flooding, sewer backups, and groundwater intrusion often require separate coverage or endorsements.

5. Unauthorized Permanent Repairs

Emergency measures to prevent additional damage are encouraged, but beginning major repairs before the insurance adjuster inspects the property could complicate the claim. Unless your insurer approves otherwise, document the damage thoroughly before permanent restoration begins.

Water Damage Insurance Claim Documentation Checklist

Proper documentation can make the claims process smoother and reduce the likelihood of disputes.

Before meeting with the insurance adjuster, gather the following:

✔ Insurance policy information

✔ Claim number

✔ Photos of all affected rooms

✔ Videos showing the extent of damage

✔ Inventory of damaged personal belongings

✔ Purchase receipts (if available)

✔ Emergency mitigation invoices

✔ Plumbing or contractor reports

✔ Temporary repair receipts

✔ Communication records with your insurance company

✔ Moisture inspection reports (if completed)

Keeping both digital and printed copies of these documents can be beneficial throughout the claims process.

How Long Do Water Damage Insurance Claims Usually Take?

The timeline varies depending on the severity of the damage, the complexity of the claim, and the insurance company’s procedures. A typical claim may involve:

Initial Report

Usually submitted within 24–48 hours after discovering the damage.

Property Inspection

An adjuster often schedules an inspection within several days, depending on claim volume and local conditions.

Damage Assessment

The insurer reviews inspection findings, repair estimates, and supporting documentation.

Settlement Decision

Straightforward claims may be resolved within a few weeks, while extensive property damage or disputes can extend the process.

Responding quickly to requests for information and maintaining organized records can help avoid unnecessary delays.

Tips to Maximize Your Insurance Settlement

While every claim is unique, homeowners can take several practical steps to strengthen their case.

Document Before Cleanup

Take detailed photographs and videos before removing damaged materials whenever it is safe to do so.

Keep Every Receipt

Save receipts for:

- Water extraction

- Temporary lodging (if covered)

- Emergency repairs

- Equipment rentals

- Cleaning supplies

Avoid Discarding Damaged Items Too Soon

Unless they pose a health or safety hazard, retain damaged items until the insurance company advises otherwise or completes its inspection.

Request Detailed Repair Estimates

Professional restoration companies can provide comprehensive estimates that clearly outline the scope of work and associated costs.

Ask Questions

If any part of your claim decision is unclear, ask your insurance representative to explain the policy language and settlement calculations.

Preventing Future Water Damage

Although unexpected incidents cannot always be avoided, regular maintenance can significantly reduce the likelihood of future losses.

Consider these preventive measures:

- Inspect plumbing annually.

- Replace aging supply lines.

- Clean gutters and downspouts regularly.

- Check your roof after major storms.

- Install water leak detection devices.

- Insulate exposed pipes before winter.

- Test sump pumps before heavy rain seasons.

- Maintain appliances according to manufacturer recommendations.

Preventive maintenance not only protects your home but may also reduce the likelihood of claim disputes related to neglect.

Frequently Asked Questions

Does homeowners insurance cover all water damage?

No. Most policies cover sudden and accidental water damage but typically exclude flooding, long-term leaks, and certain maintenance-related issues.

Should I call a restoration company before filing my insurance claim?

If there is significant water damage, contacting a professional restoration company promptly can help prevent additional damage. You should also notify your insurance company as soon as possible.

Can mold be covered by homeowners insurance?

It depends on the cause. Mold resulting from a covered water damage event may be covered, while mold caused by long-term neglect or unresolved leaks often is not.

How soon should I report water damage?

As soon as possible after discovering the damage. Prompt reporting helps support the claims investigation and may reduce complications.

What if I disagree with my insurance company’s estimate?

You can request clarification, obtain an independent repair estimate, or follow your insurer’s dispute resolution process if necessary.

Is professional water mitigation necessary?

Professional mitigation is often recommended for significant water damage because specialized equipment can detect hidden moisture, dry structural materials effectively, and help minimize the risk of mold growth.

Final Thoughts

Water damage can happen without warning, but understanding how Water Damage Insurance Claims work can help homeowners respond with confidence. Knowing what your policy covers, documenting the damage thoroughly, reporting the loss promptly, and taking reasonable steps to prevent additional damage can all contribute to a smoother claims experience.

Whether the damage stems from a burst pipe, appliance failure, or severe weather, acting quickly and staying organized can help protect both your property and your financial interests.

Professional Restoration Support When You Need It

When water damage affects your home or business, fast action is essential. Tri State Restorations provides professional water mitigation and restoration services using advanced drying equipment, moisture detection technology, and industry-recognized restoration practices. From emergency water extraction and structural drying to damage assessment and complete property restoration, the team works efficiently to help minimize further damage and support a smooth recovery process. If you’re facing unexpected water damage, partnering with experienced restoration professionals can make the restoration process faster, safer, and more manageable.