One of the biggest misconceptions about property insurance is that simply having an active homeowners or commercial property policy means every type of water damage is automatically covered.

Unfortunately, insurance policies don’t work that way.

Property insurance is a legal contract between the policyholder and the insurance company. That contract outlines not only what is covered, but also what is excluded, what is limited, and what optional coverages were purchased—or declined—when the policy was written.

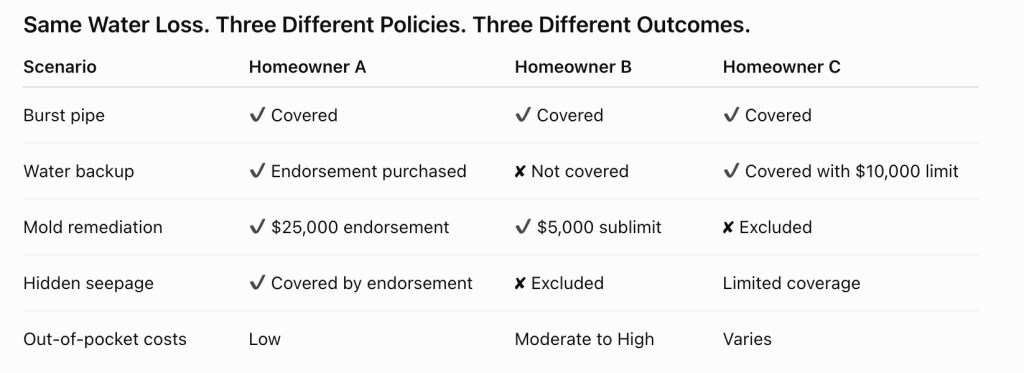

Two neighboring homes with nearly identical water losses may receive very different claim outcomes simply because their policies are different.

That’s why one homeowner may have most of their restoration covered while another may be responsible for a significant portion of the costs.

Not All Water Damage Is Treated the Same

Insurance policies often distinguish between different types of water losses. Coverage depends on the specific terms, conditions, exclusions, and endorsements contained within your individual policy. Examples may include:

- Sudden and accidental plumbing failures

- Sump pump failure

- Appliance failures

- Roof leaks caused by a covered storm event

- Water backup from sewers or drains

- Groundwater intrusion

- Long-term leakage

- Hidden seepage

- HVAC and condensate pump failures

- Condensation-related damage

- Mold and microbial growth

While these situations may all involve water damage, they are not necessarily treated the same under every insurance policy.

Understanding Endorsements and Optional Coverages

Many policyholders don’t realize that some of the most common property damage claims involve optional coverages that may or may not have been added to their policy.

Depending on the insurer and policy form, optional endorsements may include:

✔ Water Backup Coverage

✔ Hidden Water or Seepage Coverage

✔ Equipment Breakdown Coverage

✔ Service Line Coverage

✔ Increased Mold or Fungi Coverage

✔ Ordinance or Law Coverage

These endorsements often provide valuable protection—but only if they were purchased before the loss occurred.

Without them, certain portions of a claim may be limited or excluded altogether.

Mold Coverage Is Often More Limited Than You’d Expect

One area that frequently surprises property owners is mold. Many people assume that if water damage is covered, mold remediation will automatically be covered as well. In reality, many insurance policies:

- Exclude mold entirely. It is seen as a secondary damage.

- Provide only limited mold coverage.

- Cap mold remediation at a specific dollar amount.

- Cover mold only when it results from an otherwise covered cause of loss.

For example, a policy may include a $5,000 or $10,000 mold sublimit, even though the total cost of professional remediation exceeds that amount.

Every property is unique. Every policy is different.

Hidden Leaks and Long-Term Seepage

Another common source of confusion involves hidden plumbing leaks. Many policies distinguish between:

1. Sudden, Accidental Damage

These losses are often eligible for coverage, subject to the terms of the policy. Examples include:

- Burst pipes

- Water heater failures

- Supply line failures

- Sudden appliance leaks

2. Long-Term Leakage or Seepage

Many policies contain exclusions or limitations for damage that occurs gradually over time, even if the homeowner wasn’t aware of the leak. Examples may include:

- Slow plumbing leaks

- Ongoing shower pan failures

- Gradual pipe deterioration

- Months of hidden moisture behind walls leading to microbial growth

This is why identifying the cause and duration of a loss is an important part of the insurance claim process.

Why Underwriting Matters

Insurance premiums are based on risk. During underwriting, insurance companies evaluate factors such as:

- The age of the property

- HVAC systems (humidity control)

- Plumbing systems

- Roof condition

- Building materials

- Hazardous building materials such as Asbestos or Lead Paint

- Previous claims

- Geographic location (are you in a flood zone?)

- Optional endorsements selected

- Coverage limits requested

The policy that is ultimately issued reflects those underwriting decisions.

Because of that, two policies—even with the same insurance company—may provide different levels of protection.

Restoration Standards Don’t Change Because Coverage Does

Professional restoration recommendations are based on the condition of the property—not on the coverage provided by an insurance policy.

The condition of your property doesn’t change because of your insurance policy:

- If moisture is present, it still needs to be properly addressed per IICRC Standards.

- If microbial contamination is present, it still requires appropriate remediation to preserve your property’s air quality.

- If structural materials remain wet, they still need to be dried to prevent secondary damages like mold and rot.

Insurance determines what may be reimbursed. The property determines what is necessary to restore it safely.

The Questions Every Property Owner Should Ask Their Local Insurance Agent Before a Loss Occurs

Stay Proactive Not Reactive. Rather than waiting until an emergency happens, consider asking your local insurance professional the following questions about your policy:

- Do I have water backup coverage?

- Do I have coverage if my sump pump fails due to a power outage

- Is hidden leakage or seepage covered?

- Do I have mold coverage? What is my mold coverage limit?

- Are there sublimits for water damage or repairs?

- What exclusions should I be aware of?

- What deductible applies to water damage claims?

- Do I have separate coverage for contents?

Understanding your policy before a loss occurs can help eliminate surprises when you need coverage the most.

About Tri State Restorations

At Tri State Restorations, we don’t sell insurance policies, and we don’t determine insurance coverage. We help property owners and residents recover from property damage, understand the restoration process, document the condition of their property, and provide the information needed to support informed claim decisions. We believe education is one of the most valuable services we can provide—because when you understand your policy and your property, you’re better equipped to protect both.

Learn more and see why we’re known for Turning Disaster into Peace of Mind, TriStateRestores.com